Originally posted on McKinsey & Company on October 20, 2020.

The right business ecosystems can mitigate or negate the effects of structural obstacles to business building for Black business owners – and add $290 billion in business equity.

Entrepreneurship and business ownership—particularly of community-based businesses—are crucial ways to develop community wealth, for both business owners and the people they employ. Healthy Black-owned businesses could be a critical component for closing the United States’ Black–white wealth gap, which we project will cost the economy $1 trillion to $1.5 trillion (in 2018 dollars) per year by 2028. The COVID-19 crisis, however, has further stressed Black-owned businesses and may cause the racial wealth gap to widen. This gap includes a $290 billion—and growing—opportunity to grow overall wealth by achieving revenue parity between Black- and white-owned businesses in addition to providing aid to small and medium-size businesses (SMBs)—those with up to 500 employees—with nonwhite owners.1

Black business owners have been disproportionately affected by the pandemic-linked economic downturn, partly because they were more likely to already be in a precarious position, including more likely to be located in communities with business environments that are more likely to produce poor business outcomes. Indeed, about 58 percent of Black-owned businesses were at risk of financial distress before the pandemic, compared with about 27 percent of white-owned businesses.2 The pandemic contributed to tipping 41 percent of Black-owned US businesses into closure from February to April 2020.3 More than 50 percent of the owners of surviving Black businesses surveyed in May reported being very or extremely concerned about the viability of their businesses. This concern may be linked to having a more difficult time accessing credit since the COVID-19 crisis began; 36 percent of Black business owners responding to the survey said they had experienced this, compared with 29 percent of all respondents.4

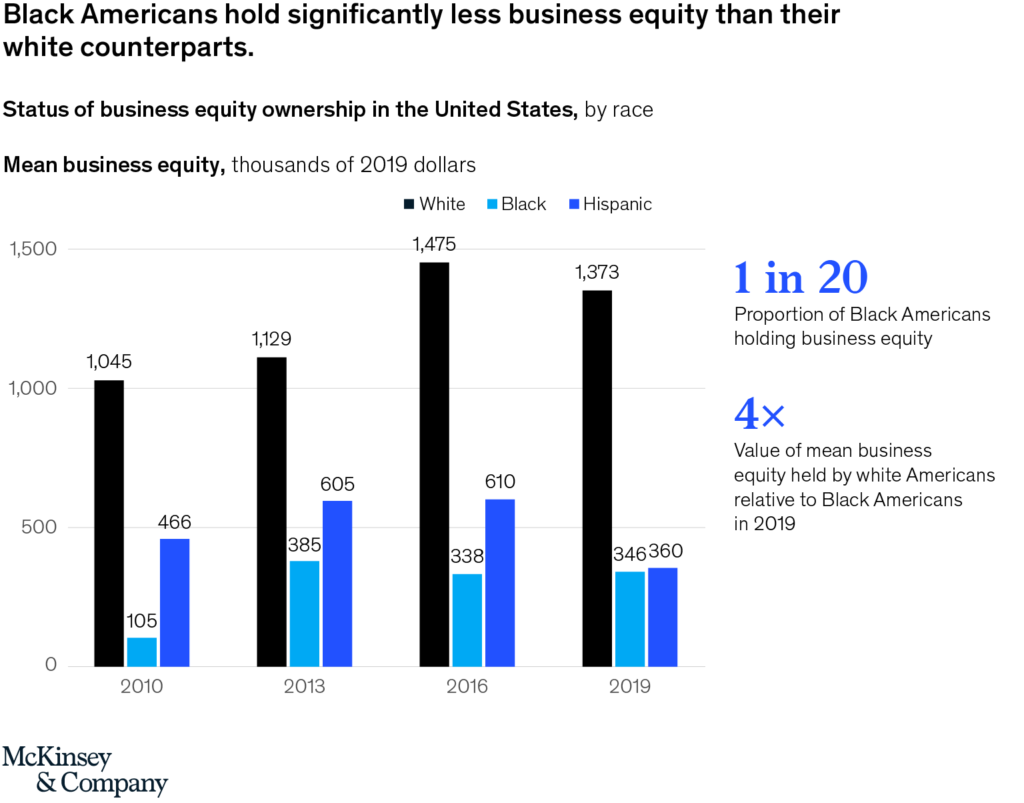

Black Americans have never had an equal ability to reap the benefits of business ownership. While about 15 percent of white Americans hold some business equity, only 5 percent of Black Americans do. Among those with business equity, the average Black American’s business equity is worth about 50 percent of the average American’s and a third of the average white American’s (Exhibit 1).5

Black-owned businesses also tend to earn lower revenues in most industries and are overrepresented in low-growth, low-revenue industries such as food service and accommodations.

This gap in business activity contributes to an overall lower level of prosperity for Black families: the median white family’s wealth is more than ten times the wealth of the median Black family’s. This disparity is also a lost opportunity for the US economy as a whole. If existing Black-owned businesses reached the same average revenue as their white-owned industry counterparts (excluding publicly held companies), the result would be an additional $200 billion in recurring direct revenues, which could equal about $190 billion in additional GDP, or a roughly 1 percent increase in 2017 GDP. (For our analytical approach, see sidebar “Quantifying the impact of revenue parity.”)

Before the pandemic, the average American held 15.3 percent of his or her wealth in business equity, with a mean value of $147,000. SMBs constituted 99 percent of US businesses and were responsible for 62 percent of the net increase in private-sector jobs from 1993 to 2017.6 Entrepreneurship and an ability to start new businesses matter significantly here, as more than 50 percent of this net increase was the result of the formation of new businesses, defined as those less than 3.5 years old.7

Our analysis mapped barriers throughout the entrepreneurial pathway: ideation and starting up, sustaining, scaling, and exiting (see sidebar “Entrepreneurial pathway: Building a business, from ideation to exit”).

We focus here on the systemic barriers that hinder Black entrepreneurs’ efforts to ideate and start and sustain local businesses—that is, community-based SMBs that are part of existing supply chains.8 We then outline interventions that can counteract the effects of these obstacles, particularly opportunities for coordinated efforts. Indeed, US institutions need to repair Black business owners’ trust in the business ecosystem—particularly in companies in financial and business services.9 This historic lack of trust may be slowing business creation; research shows that Black business owners may believe that they need to be better qualified than their white counterparts: 30 percent of Black owners of employer firms (businesses with at least one paid employee) hold an advanced degree, which is true of 22 percent of their white peers.10

A silver lining of COVID-19 and the racially charged violence in 2020 may end up being that some large companies have now launched programs to support Black-owned businesses: a major social media company dedicated $40 million in grants to support Black-owned US businesses with 50 or fewer employees11 ; a financial services firm pledged $1.15 billion, including $350 million in procurement spending on Black-owned businesses, to close the racial wealth gap.12 However, these individual actions will not in themselves be enough to effect the needed change. For this work to have a systemic impact, entire business ecosystems will need to be involved. Once successful, however, this effort would benefit not only the US economy but US society as a whole.

A silver lining of COVID-19 and the racially charged violence in 2020 may end up being that some large companies have now launched programs to support Black-owned businesses.

Barriers to business building for Black entrepreneurs

Throughout the business-building process, Black business owners face economic, market, sociocultural, and institutional barriers, which are all linked to racial discrimination in the United States. Economic barriers relate to disempowerment and the costs of low starting levels of capital—for individuals, families, and communities. Market barriers result from unaddressed needs, often related to challenges of access—to capital, expertise, and services. Sociocultural barriers encompass the biased and exclusionary ways in which Black entrepreneurs are more likely to be blocked from gaining social capital, such as helpful relationships that make up business networks. Finally, institutional barriers are supported by the systems in which Black-owned businesses operate and include factors as basic as their locations.

Ideating

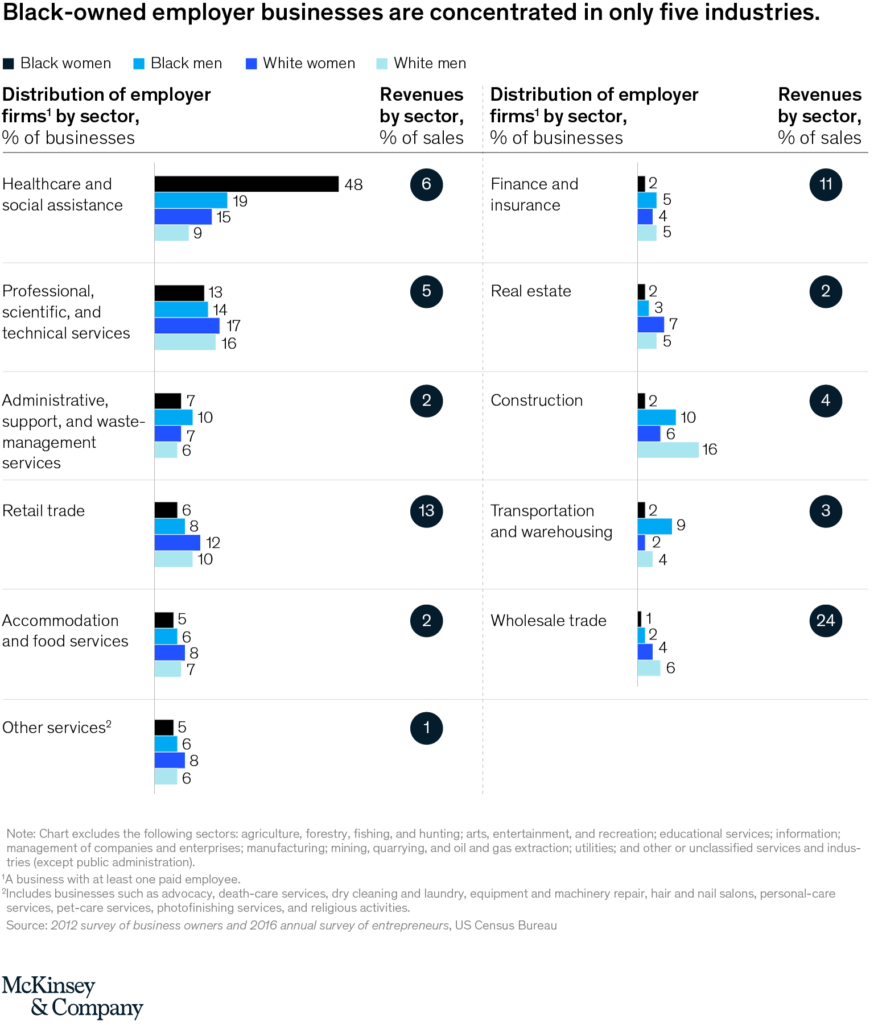

Black entrepreneurs tend to make decisions in the business-ideation stage that are likely to keep their businesses small. Black entrepreneurs generally pursue businesses in less lucrative sectors. Only five industries represent employer businesses (that is, businesses that employ paid employees) owned by 74 percent of Black women business owners and 62 percent of Black male business owners: healthcare and social assistance; professional, scientific, and technical services; administrative support and waste management services; construction; and transportation and warehousing (Exhibit 2).13

These sectors represent only 20 percent of business revenues overall. Meanwhile, although wholesale businesses represent 24 percent of business revenues, only 1 percent of Black women and 2 percent of Black men who are entrepreneurs are in the sector (see sidebar “Uphill climb for Black women in entrepreneurship”).14

Location can also limit Black entrepreneurs’ business potential. Sixty-five percent of Black Americans live in 16 states that are below the US average on indicators of economic opportunity.15 Within their communities, Black Americans are also disproportionately concentrated in economically disadvantaged neighborhoods. Black entrepreneurs from these communities are less likely than their white peers to have exposure and access to lucrative business opportunities.

Black entrepreneurs might also lack access to the networks and relationships that could help them make optimal business decisions. Research on New York–based start-ups shows that founders who are mentored by top-performing entrepreneurs are three times more likely than their co-located peers without mentors to become top performers themselves.16 Outside the start-up world, a knowledgeable contact may help a prospective entrepreneur make decisions such as whether to buy a franchise for up-front capital or to build an independent business.

Crucially, Black entrepreneurs struggle more to secure capital and access to credit. Even with strong personal credit, Black business owners and other entrepreneurs from marginalized groups are about half as likely as their white counterparts to receive full financing.17 Friends and family may not be able to contribute capital either. Most Black families surveyed said that they didn’t know anyone who could lend them $3,000.18

Starting up and sustaining

The focus of the start-up and sustain phases of entrepreneurship should be on ensuring the business’s survival and increasing its profitability. However, Black entrepreneurs’ mistrust of institutions—based on their experiences and knowledge of the United States’ history of discrimination—can make them wary of using potential resources outside their communities. Combined with a lack of informal and geographic connections to such resources—including venture-capital networks—this tendency can isolate Black entrepreneurs from potential sources of support.19 (For an overview of the public sector’s attempts at closing the gap between Black- and white-owned businesses—and their pitfalls—see sidebar “Legislating for more equitable business outcomes.”)

Only 4 percent of Black American businesses survive the start-up stage, even though 20 percent of Black Americans start businesses.20 Even if they survive the start-up stage, Black-owned businesses still disproportionately struggle with debt and raising capital in addition to challenges such as a lack of helpful relationships in the business community. Indeed, participants in focus groups said that they feel that their race—and sometimes age and gender—makes loan officers hesitant to lend to them.21 Such obstacles make Black-owned businesses less likely to survive and grow.

Start-up capital is associated with better business performance,22 but Black entrepreneurs have less of it. Black entrepreneurs start their businesses with about $35,000 of capital, white entrepreneurs $107,000.23 As a partial consequence, Black-owned businesses report higher levels of debt relative to revenues. Almost 30 percent of Black-owned businesses spent more than 50 percent of their revenues to service their debt in 2019.24 Indeed, Black entrepreneurs are three times as likely as white entrepreneurs to say that a lack of access to capital negatively affects their businesses’ profitability and almost twice as likely to cite the cost of capital.25 This lack of capital occurs even though the requirements for Black applicants are more stringent. In one study, 73 percent of Black loan applicants were asked to provide financial statements for their businesses, compared with 50 percent of white applicants with comparable profiles. In addition, 31 percent of Black applicants were asked to provide their personal W-2 forms. No white applicants received such a request.26

Black entrepreneurs are three times as likely as white entrepreneurs to say that a lack of access to capital negatively affects their businesses’ profitability and almost twice as likely to cite the cost of capital.

These interactions with financial institutions are consistent with findings that nonwhite ownership of a business is a strong predictor of loan denial outside of majority-nonwhite communities.27 However, simply being located in a co-ethnic market—where community members, customers, and business owners are of the same ethnicity—results in lower revenue, even for businesses of comparable quality.28 Indeed, research shows that even when they have better Yelp reviews, businesses in majority-Black communities have lower revenues than those outside majority-Black communities. Black-owned businesses are in a double bind that results in missing revenues.

Black entrepreneurs can also have difficulty accessing expertise and business services. Black owners of employer firms, which are more likely to benefit from services such as legal and financial advisory, are less likely to seek them out. Only 58 percent of Black owners sought professional services, for reasons including expense, inaccessibility, and mistrust, compared with 70 percent of white owners.29

Business networks can support Black entrepreneurs, but Black entrepreneurs are less likely to know and hear about relevant networks that can help support and promote their businesses. Indeed, Black entrepreneurs are likely to be excluded from receiving information about high-potential opportunities, even though focus-group participants said that they would like to connect with a variety of business professionals and mentors. This exclusion translates into fewer connections to formal hubs,30 such as banks and venture-capital funds, and from informal networks. One sign of this disconnection is that corporate and government procurement programs that target Black-owned businesses tend to be underused. The Minority Business Development Agency (MBDA) found in 2016 that Black-owned businesses saw less utilization relative to their availability than white-owned businesses did in the same industries. The median share of contract dollars awarded to Black-owned businesses across five key industries—architecture and engineering, construction, goods and supplies, professional services, and other services—was 4 to 44 percent of contractors’ availability, compared with 49 to 61 percent for white-owned businesses.31

The aggregate barriers to starting and sustaining a Black-owned business translate structural bias into less access to capital, lower revenue, and dimmer prospects for business growth. The mainstream financial system’s role in those barriers has helped to maintain Black Americans’ distrust of the financial sector as well as fear of debt.32

Interventions

Insufficient access to capital, knowledge, and support ultimately leaves many Black entrepreneurs less economically mobile and limits the potential of entrepreneurship to grow wealth for Black families and communities. Interventions to tackle these barriers will require public-, private-, and social-sector stakeholders to evaluate current business ecosystems and rebuild them to be equitable and more supportive for Black business owners. In particular, local anchor institutions such as hospitals and universities can take the lead on collaborating with the public and social sectors to coordinate the work of disparate organizations. Local economic-development institutions, community development financial institutions, chambers of commerce, and other government agencies such as the Small Business Administration or MBDA are already engaged in these activities. But because anchor institutions are tethered to their communities, they stand to reap long-term benefits from investing in more equitable—and healthier—business communities.

Indeed, this work requires instituting policies that create more equitable outcomes in addition to assuring equitable access to capital. Black leaders’ input can help create positive experiences and build Black entrepreneurs’ trust in institutions and ecosystems that have felt exclusionary. In addition, the private and social sectors should help Black-owned businesses build capabilities and facilitate knowledge sharing. Expanded opportunities for mentorship (advisory) and sponsorship (advocacy) can further solidify bonds between Black entrepreneurs and other stakeholders in business ecosystems.

Implement policies that produce equitable outcomes

The public, private, and social sectors can all participate in removing institutional barriers for Black-owned businesses. Stakeholders could ensure that laws, policies, and practices are designed to produce equitable opportunities and outcomes.

Policy makers, industry groups, affinity groups, and coalitions of stakeholders could enforce laws and policies aimed at preventing inequitable processes and outcomes. After a review of the current laws and policies and their effects, stakeholders could consider updating antidiscrimination policies. Crucially, stakeholders could set up—or support—internal and external watchdog groups dedicated to creating research on equity in processes and policy outcomes.

In addition, procurement practices, especially at anchor institutions and large organizations, can evolve to be more inclusive of Black-owned businesses. Besides dedicating funds to procurement from Black-owned businesses, large organizations could simplify their minority-supplier certification processes so that they can take on new suppliers more quickly. Organizations should also dedicate funding to supplier-development programs that can help Black-owned suppliers better participate in supply chains.

Once their supplier programs are established, organizations should track their procurement spending with important categories of suppliers and make the data more widely available to track progress and promote accountability. For instance, one North American bank committed to tracking its spending with diverse suppliers, the number of minority-certified suppliers it engages, and the number of requests for information and proposals to these suppliers.33 This work is especially urgent during the pandemic-linked economic crisis, and entities that have an interest in keeping business ecosystems vibrant may be able to lead the effort.

Enable equitable access to capital

To overcome economic barriers, Black-owned SMBs need direct investment or in-kind equity contributions, including grants, subsidies, loans, and revenue-participation agreements. Direct investment is especially important during the COVID-19 crisis. Our analysis suggests that an additional $7.6 billion to $15.4 billion in liquidity for Black-owned SMBs in the 2020–21 time frame—less than 3 percent of the $659 billion authorized under the Paycheck Protection Program—could preserve 460,000 to 815,000 jobs,34 for an average of $9,325 to $33,478 per job.

An additional $7.6 billion to $15.4 billion in liquidity for Black-owned SMBs in the 2020–21 time frame—less than 3 percent of the $659 billion authorized under the Paycheck Protection Program—could preserve 460,000 to 815,000 jobs, for an average of $9,325 to $33,478 per job.

The public and private sectors’ immediate priority during the COVID-19 economic crisis has been to provide SMBs with grants and loan deferrals. However, increasing the availability of financial resources, particularly start-up and expansion capital, for Black entrepreneurs, will be crucial to improving business owners’ experience and replenishing the pipeline of growing businesses. For example, banks, conventional and social-impact investors, foundations, and public programs could make more capital available to Black-owned businesses. Possible programs include ones that make extending capital to Black-owned businesses less risky through measures such as guaranteeing funds and programs that help entrepreneurs from marginalized backgrounds acquire more capabilities. A short-term counterweight to the effects of bias in the loan process could be conducting fewer in-person transactions. Indeed, Black entrepreneurs are already more likely to borrow online, where their race may be less salient.35 A program for small-business investment companies that provides high-growth small businesses with capital and R&D funding could also accelerate the growth of Black-owned businesses that hold intellectual property and may foster Black entrepreneurship in high-growth industries.

A network of volunteer professional services providers and coaches could help Black-owned businesses navigate the process of attaining loans, grants, and other affordable capital, including from large corporations and nonprofit organizations.36

In addition to continuing the long-term project of cultivating Black leaders in positions of influence on capital funding, cross-sector entities could convene and support a consortium of Black fund managers to participate in issuing and managing debt and equity investments in small businesses. The SBA already licenses small-business investment companies that guarantee funds that invest in SMBs. Increasing the share of Black fund managers in this program and simultaneously investing in Black managers—and the pipeline of Black leaders—in the private sector could have compounding effects.

Build business capabilities and facilitate knowledge sharing

To overcome market barriers, Black-owned SMBs need support for building capabilities and sharing a greater amount of knowledge. Black service providers, compensated by organizations working to support equity in entrepreneurship, can lead these capability-building efforts. This work would protect and strengthen Black-owned businesses and build business networks with Black-owned SMBs as hubs.

The private and social sectors—particularly anchor institutions—could provide resources, including help with reskilling and upskilling Black-owned businesses’ workers, to make Black-owned SMBs nimbler. For instance, a major social-media platform built a resource hub to provide businesses with industry-specific information they could use during the pandemic. Similarly, on-the-job training and free web-based courses are both resources that can be easily shared among multiple—indeed, many—businesses. Business-services providers could also facilitate digital transformations to help businesses identify new market opportunities.

Finally, digital capabilities will increase Black entrepreneurs’ share of opportunities, but the corresponding business services are long-unmet needs. Many Black-owned businesses lack the resources to hire service providers that can help them digitize their businesses, but private-sector and social-sector organizations can provide free technology services and managerial assistance. Free or subsidized installation, tech support, and staff training can help Black-owned businesses acquire more digital capabilities and become more able to share this knowledge with other Black-owned businesses in their communities.

Expand opportunities for mentorship and sponsorship

Representation and participation in networking, mentorship, and sponsorship programs can help Black entrepreneurs overcome some sociocultural barriers. The private sector should take the lead by building more inclusive teams. Managers at every level should consciously develop—and sponsor the careers of—more Black leaders to counteract the effects of structural bias. Indeed, only about 3 percent of current Fortune 100 company CEOs are Black, and fewer than 4 percent of leaders with responsibility for departments’ profit and loss—roles that tend to accelerate career progression—are Black.37 Moreover, unconscious bias can affect mentorship and sponsorship, because humans tend to gravitate toward mentoring people they view as similar to themselves.38

Community programs can help Black entrepreneurs connect with role models and commercial networks that can help Black prospective entrepreneurs pursue business ownership with more confidence and support. For instance, the private and social sectors could facilitate networking and partnerships between established businesses and compatible start-ups.

An investment in more business ecosystems that provide Black business owners equitable access to resources and opportunities can unlock part of the $1 trillion to $1.5 trillion in annual GDP that would come from closing the racial wealth gap. More important, by making social and economic institutions supportive of a wider swath of people, stakeholders can rectify the mistrust that has developed between Black entrepreneurs and institutions. That restorative effect, along with economic gains, could be a step forward for US society.

ABOUT THE AUTHOR(S)

David Baboolall and Nina Yancy are consultants in McKinsey’s New York office; Kelemwork Cook is a consultant in the Cleveland office; Nick Noel is a consultant in the Washington, DC, office; and Shelley Stewart is a partner in the New Jersey office.

The authors wish to thank Katie Chen, Michael Chui, JP Julien, Mike Kerlin, Michael Lazar, Ricardo Pena, and Duwain Pinder for their contributions to this article.